There is a quiet revolution happening inside the grocery shopping cart. For decades, supermarkets and food brands made their money by encouraging consumers to buy more, eat more, and snack often. But new data from June 2026 (Kantar WorldPanel «The Ripple Effect: How GLP-1 Medications are Reshaping the UK Grocery Landscape» (3rd Annual Insights Report)) shows that a powerful medical trend is breaking this classic business model.

Weight-loss medications – especially GLP-1 drugs like Wegovy, Mounjaro, and Ozempic – are no longer just private medical treatments. They have become a massive disruptive force in the Fast-Moving Consumer Goods (FMCG) industry.

In this deep dive, we look at how these drugs are creating a “small appetites economy”. We will explore the shocking numbers behind this trend, reveal an unexpected boom in the oral care aisle, and give retail professionals practical tips on how to adapt to this new consumer.

The Macroeconomic Shockwave: Jabs Are Shrinking Grocery Bills

Let us start with the most important fact: consumers on GLP-1 medications are spending much less money on food.

In Great Britain, the number of households with at least one active GLP-1 user has nearly tripled in just two years. In 2024, only 2.3% of households had a user. By 2025, that number rose to 4.1%. Today, in June 2026, it has jumped to 6.3% of all British households. This means about 1.9 million adults in Britain are now using these drugs.

This rapid change has taken £780 million off grocery retail tills. When a consumer starts taking these medications, their shopping habits change immediately. On average, a household with a GLP-1 user spends £418 less per year on groceries than a similar household without a user. Across the country, this adds up to 299 million fewer product packs bought.

Controversial Statement:

Some retail analysts previously argued that weight-loss drugs were a minor trend that would only affect ultra-wealthy consumers. The June 2026 data completely disproves this. With nearly 2 million British adults on these medications, GLP-1 adoption is now a mainstream macroeconomic event that is directly shrinking supermarket revenues.

This trend is also hitting continental Europe. In Spain, data from the consulting firm Lantern in March 2026 shows that GLP-1 treatments now have about 500,000 active users and are growing at double-digit rates. This growth is happening because 55.8% of Spanish adults are overweight or obese.

In 2025, sales of these weight-loss medicines in Spain went over €840 million. This was a massive 75% increase compared to the previous year, with 7.2 million treatment units sold.

A Closer Look at the Demographics

Who is the typical GLP-1 consumer? The data shows a very clear gender split. In Great Britain, women make up 77% of active users, while men account for only 23%.

Another major shift is why people take these drugs. Originally, these medicines were for type 2 diabetes. Today, 68% of users take them strictly to lose weight.

In fact, 26% of respondents say they would use a GLP-1 drug to lose weight even if they did not have any major health issues. This shows that these drugs have transitioned from essential medical therapies into lifestyle products.

| Market Metric | Great Britain (2026 Data) | Spain (2026 Data) |

|---|---|---|

| Household Penetration | 6.3% (Up from 2.3% in 2024) | Estimated 1.2% to 1.5% of adults |

| Active Adult Users | ~1.9 million adults | ~500,000 active users |

| Total Financial Impact | -£780 million in grocery sales | +€840 million in pharmacy sales (2025) |

| Change in Household Spend | -£418 per year vs. non-users | -3.1% in basket value / -3.8% in volume |

| Core User Demographics | 77% female / 23% male | Concentrated in higher income groups |

| Main Reason for Use | 68% for weight loss; 26% for lifestyle weight loss | General weight management (18-20 kg average loss) |

Neuro-Retail: Understanding the Death of Impulse Buying

To understand why these shopping carts are shrinking, we have to look at how these drugs affect the human brain.

GLP-1 medications mimic natural hormones that tell the brain you are full. This does two things: it slows down how fast the stomach empties, and it stops what scientists call “food noise”. Food noise is the constant, background urge to snack, eat sweets, or think about the next meal.

According to the data, 54% of GLP-1 users report a massive drop in cravings and food noise. Furthermore, 11% of users say they no longer enjoy their favorite indulgent foods and drinks at all.

This biological change is destroying the traditional “impulse buy” model that supermarkets rely on for high profit margins. If a consumer does not experience food noise, they will not grab a chocolate bar at the checkout till.

Instead, 52% of users now describe their eating habits as “mindful”. This means they eat only when their body feels physical hunger, rather than eating out of habit, boredom, or stress.

Strategic Insight:

For decades, snack manufacturers designed colorful packaging and run price promotions to trigger impulse buys. Mindful eaters are immune to these triggers. They shop with a list and buy with strict nutritional intent. FMCG brands must stop trying to tempt these shoppers and instead start explaining how their products solve specific nutritional needs.

Winners and Losers in the Shopping Basket

The drop in food purchases is not equal across all categories. Traditional junk foods and indulgent treats are experiencing a severe decline.

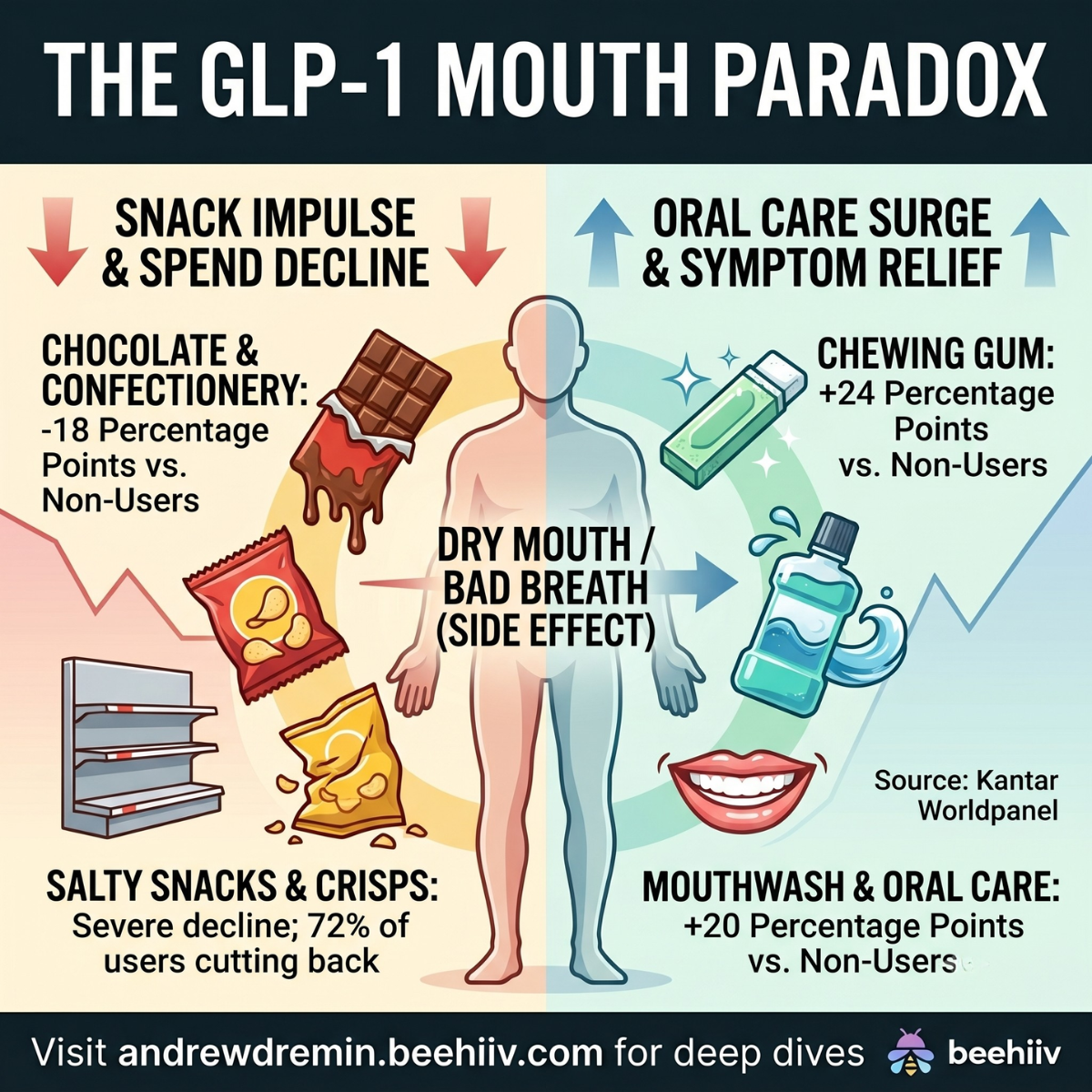

In Great Britain, 75% of GLP-1 users have cut back on chocolate, and 72% have cut back on crisps (potato chips). Spend data confirms this: chocolate sales in GLP-1 households fell 18 percentage points faster than in non-user households since starting the treatment.

The Spanish Lantern study shows the exact same trend. When Spanish consumers start using GLP-1s, their purchases of chocolate bars drop by 17.9%, and salty snacks/crisps drop by 13.5%.

Even more interesting is the impact on alcohol. Because these medications dampen the brain’s reward systems, users lose interest in drinking. In Spain, wine purchases among GLP-1 users fell by 12.5%, and beer purchases dropped by 11.4%.

However, healthy, basic food categories are winning. Spanish users increased their spending on:

- Olive oil: +24.8%

- Peas: +5.9%

- Fresh fruits and eggs: +1.4%

| Product Category | Spend Shift (UK Households) | Spend Shift (Spain Households) | Core Behavioral Driver |

|---|---|---|---|

| Chocolate & Confectionery | -18 percentage points vs. non-users | -17.9% in volume | 54% reduction in cravings; no more chocolate impulse buys |

| Salty Snacks & Crisps | 72% of users are cutting back | -13.5% in volume | Shift toward mindful eating and away from heavy, salty snacks |

| Alcohol (Wine & Beer) | Notable downward trend | -12.5% Wine / -11.4% Beer | Brain’s reward pathways are dampened; less tolerance for empty calories |

| Mouthwash & Oral Care | +20 percentage points vs. non-users | Positive baseline growth | Combating dry mouth and bad breath caused by the medication |

| Chewing Gum | +24 percentage points vs. non-users | High transactional growth | Mechanically stimulating saliva production to fight dry mouth |

| Basic Whole Foods | Stable / slightly positive | +24.8% Olive Oil / +5.9% Peas / +1.4% Fruits & Eggs | Consumers focus on raw ingredients and high-nutrient meals |

The “GLP-1 Mouth” Paradox: A New Goldmine in the Toothbrush Aisle

While food and beverage companies are losing billions of pounds, a highly profitable business has opened up in the personal care aisle. This is what analysts call the “GLP-1 Mouth” Paradox.

On social media, consumers frequently complain about a dry mouth, a metallic taste, and bad breath after taking weight-loss medications. This is not just a cosmetic issue; it is a direct physical side effect of the drugs.

The Clinical Explanation

GLP-1 receptors are found all over the human body, including in our salivary glands. When a patient takes semaglutide or tirzepatide, the drug actively reduces the flow of saliva in the mouth.

Saliva is the mouth’s natural defense system. It washes away food particles, neutralizes acids, and kills harmful bacteria. When saliva flow drops, it causes a condition called xerostomia (severe dry mouth). Without saliva, bacteria grow rapidly, leading to:

- Halitosis: Severe, chronic bad breath.

- Tooth Decay: Rapid-onset cavities, even in people who historically had healthy teeth.

- Gum Disease: Painful, bleeding, and inflamed gums.

Furthermore, many GLP-1 users experience regular nausea, acid reflux, or vomiting as their bodies adjust to the medication. This acid exposes teeth to extreme wear, stripping away enamel.

Dehydration also plays a massive role. Because these drugs suppress both hunger and thirst signals, users often forget to drink water, which stops salivary glands from working even more.

Finally, because users are eating smaller meals, they spend less time physically chewing. Chewing is the physical trigger that tells the body to produce saliva. Less chewing means a drier mouth.

The Retail Impact

To fight these uncomfortable symptoms, GLP-1 users are buying oral care products at an unprecedented rate.

- Mouthwash Sales: GLP-1 households have recorded a 20 percentage point increase in mouthwash spending compared to non-user households. However, users quickly learn that standard, alcohol-based mouthwashes make the problem worse because alcohol dries out oral tissues. Instead, they are searching for specialty mouthwashes that contain soothing enzymes and humectants to keep the mouth wet.

- Chewing Gum Sales: Chewing gum spend has skyrocketed by 24 percentage points among user households. Users chew gum to physically force their salivary glands to work. Sugar-free gums made with xylitol are the big winners here, as xylitol fights cavity-causing bacteria while refreshing breath.

- High-Value Oral Tools: Retailers are also seeing sales growth in advanced electric toothbrushes, enamel-repair toothpastes, and water-flossers.

How Brands and Supermarkets Are Re-Engineering Their Portfolios

Supermarkets and brand owners are not sitting still. They realize that if consumers are eating less, they must focus on nutritional density and portion control to survive.

When a consumer’s stomach capacity is limited, they cannot afford to waste their appetite on empty calories. They want high-quality protein to protect their muscles from breaking down during rapid weight loss. They also need high dietary fiber to combat severe constipation, which is a common side effect of slowed digestion.

As a result, 40% of users demand smaller portion sizes, and 26% want dedicated, medically friendly product sections in supermarkets.

Here is how major industry players are adapting to this demand:

1. Supermarket Innovations

- Ocado: The UK online grocer has created a dedicated virtual “weight management” aisle. This makes it easy for GLP-1 users to find high-protein, high-fiber, and low-sugar foods without having to search through thousands of standard products.

- Marks & Spencer (M&S): This premium retailer has launched a new range of “nutrient-dense” meals. These dishes are packed with high-quality protein and essential vitamins but are packaged in modest, easy-to-finish portions.

- Morrisons: Morrisons created its own-label “GLP-1 friendly” ready meals. A key product is a chicken casserole that weighs exactly 280 grams – perfectly sized for a suppressed appetite so that no food is wasted.

- Asda, Sainsbury’s, and Co-op: These retailers are expanding their high-protein and high-fiber shelves. Sainsbury’s has reported that GLP-1 users are buying significantly more fresh produce and prebiotic-rich items to support their gut health.

- Boots: The pharmacy chain has shifted its marketing away from narrow weight-loss standards. Its campaigns now highlight general wellness, sleep, muscle strength, and gut health, matching the broader health goals of the GLP-1 consumer.

2. Brand Portfolio Changes

- Nestlé (Vital Pursuit): In a major first-mover play, Nestlé launched a frozen food brand called Vital Pursuit. These meals are high in protein, rich in fiber, and perfectly portioned to help GLP-1 users meet their daily nutritional needs.

- Lactalis (:ratio Pro-Fiber): Released in late 2025, this yogurt is specifically formulated for weight-loss patients. Each serving delivers 20 grams of protein and 10 grams of dietary fiber, helping users bridge the “fiber gap” caused by eating less food.

- Danone (Oikos Fusion): This high-protein dairy snack features 5 grams of prebiotic fiber, vitamin D, and leucine to help preserve muscle mass under a calorie-restricted diet.

The Patent Battleground and the Affordability Wall

Despite the rapid rise of these medications, there is a major commercial barrier: price.

In 2026, 41% of users stopped taking their GLP-1 treatments simply because they could no longer afford them. These drugs can cost several hundred pounds a month out-of-pocket, meaning future retail disruption is heavily tied to health insurance coverage and generic manufacturing.

The High Cost of Staying Thin

In both Great Britain and Spain, public healthcare systems do not fund these drugs for general weight loss, forcing patients to pay private cash prices.

- United Kingdom: The daily oral tablet format of semaglutide was approved by the MHRA on 11 June 2026, but it is not funded by the NHS for weight loss. In private clinics, injectable Wegovy costs between £79.97 and £97.00 per month for the lowest dose, climbing to £285.97 or £297.00 per month for the highest maintenance dose. Off-label oral alternatives cost between £150 and £400 per month.

- Spain: Wegovy is sold in pharmacies with a strict medical prescription but has zero coverage from the Seguridad Social (National Health System) for obesity. The starter dose costs €179.89 per month, while the maximum maintenance dose costs €223.64 per month.

The Transition to Daily Pills

On 11 June 2026, the UK’s MHRA approved the country’s first daily oral tablet for weight management. Early data from the United States (where the pill launched in January 2026) shows that oral tablets are a massive game-changer. Within eight weeks of the US launch, the oral tablet captured one-third of all new weight-loss prescriptions, and two-thirds of those patients had never used an injectable drug before.

Strategic Insight:

The move from weekly injections to a simple daily pill removes a massive psychological barrier for needle-hesitant consumers. This is expected to trigger a second major wave of consumer adoption by 2027, potentially doubling the number of active users in Europe.

However, taking the oral tablet requires a very strict fasting routine to allow the body to absorb the medicine. The clinical administration rule is mathematically precise:

Fasting Duration≥8 hours⟹Ingest Tablet Whole with a Sip of Water⟹No Food/Drink≥30 minutes

Because users cannot eat or drink anything (including coffee or breakfast) for at least 30 minutes after taking the pill, this routine is expected to completely eliminate the traditional “morning grab-and-go” breakfast run for millions of consumers.

The Patent Wars: When Will Generics Arrive?

The long-term price of GLP-1 drugs depends entirely on patents.

- Liraglutide (Victoza / Saxenda): The compound patents expired in November 2024. This has allowed generic manufacturers to launch cheap daily injections like Nevolat, which retail for around £94.97, offering a much more affordable entry point.

- Semaglutide (Ozempic / Wegovy): The patent situation here is highly complex and controversial. The main compound patent should technically expire in March 2026. However, in the US and Europe, Novo Nordisk used Patent Term Extensions (PTE) to push this protection to December 2031. In addition, they hold 49 follow-on patents covering specific dosing schedules, formulations, and mechanical injection pens that extend protection until 2042.

- The “Device Trap”: Crucially, 54% of all patents listed for GLP-1 products are for the delivery pens, not the active chemical itself. This creates a massive legal barrier that prevents generic drugmakers from selling simple syringes.

- Global Divergence: Countries like India, China, and Brazil do not allow these extensive patent extensions. As a result, semaglutide patents are expiring in these emerging markets in 2026. This will allow local generic manufacturers to flood those countries with incredibly cheap weight-loss options, accelerating adoption in Asia and Latin America years before the US or Europe see cheap generics.

Actionable Lessons for Retail and FMCG Professionals

For retail leaders and brand owners, the rise of the GLP-1 consumer is not a trend you can ignore. However, it is also not a death sentence for your volumes.

Here are three concrete, real-world strategies to implement today:

1. Adopt “The Power of One” Packaging Strategy

In convenience stores, GLP-1 users are driving a trend called “the power of one”. Because they no longer experience food noise, they rarely buy large multi-packs or family-sized bags of treats. Instead, when they experience a true physical craving, they prefer to buy a single, premium serving of their favorite treat.

- What to do: Food brands must redesign their packaging architectures. Shift your focus away from low-margin bulk family packs and invest heavily in high-margin, single-serve premium packaging. This allows you to protect your profit margins even as physical volumes decline.

2. Capitalize on “GLP-1 Mouth” with Co-Bundling

Oral care brands and functional confectionery brands should actively build product bundles designed to solve the physical symptoms of these medications.

- What to do: Do not just sell mouthwash or chewing gum in isolation. Create “Dry Mouth Comfort Packs” that pair non-drying, enzyme-based mouthwashes with sugar-free xylitol mints and gums. Position these bundles directly next to pharmacy counters, weight-management aisles, or health food sections.

3. Build Proactive “Gut-Friendly” Store Environments

With 26% of users asking for dedicated store sections, supermarkets have a massive opportunity to create physical and digital wellness ecosystems.

- What to do: Create online search filters and in-store “Metabolic Wellness” endcaps. Group high-protein foods, fiber supplements, and oral therapeutics together. When users search for weight-management products on your app, automatically suggest fiber-dense meals and dry-mouth solutions.

Conclusion: The Path Forward

The “small appetites economy” is not a temporary phase. It represents a permanent, structural change in how millions of humans interact with food, health, and wellness.

The retailers and brands that succeed in this new era will not be those that try to force old habits onto consumers. Success will belong to the agile players who recognize these biological shifts, embrace the power of portion control, and capture the highly profitable spaces left behind by shrinking appetites.

Medical Disclaimer

This article is for informational and educational purposes only. It is intended to analyze retail, consumer behavior, and industry trends, and should not be taken as medical advice. If you are considering GLP-1 medications or have questions about their health effects, side effects, or administration, always consult with a qualified doctor or healthcare professional. Do not make any medical decisions or start, stop, or alter any medication without professional medical guidance.

Leave a Reply