16 years old. That is becoming the global benchmark age where regulators want to ban teenagers from buying energy drinks.

Look at the global data. In early 2026, Spain announced a nationwide ban on selling energy drinks to anyone under 16, and restricted high-caffeine versions for under-18s. Their market is huge: 105 million liters purchased last year alone. Poland enacted a strict ban for under-18s starting January 1, 2026, with sellers facing fines of 2,000 PLN. The UK government is pushing a similar ban for under-16s, explicitly citing sleep disruption and cognitive impact. Kazakhstan went even further, banning sales for anyone under 21.

The target is clear and unified across borders: packaged high-caffeine cans.

But look at the massive contradiction.

A 15-year-old can still walk into any high-street coffee shop, order a double espresso, and walk out. Zero restrictions. Zero ID checks.

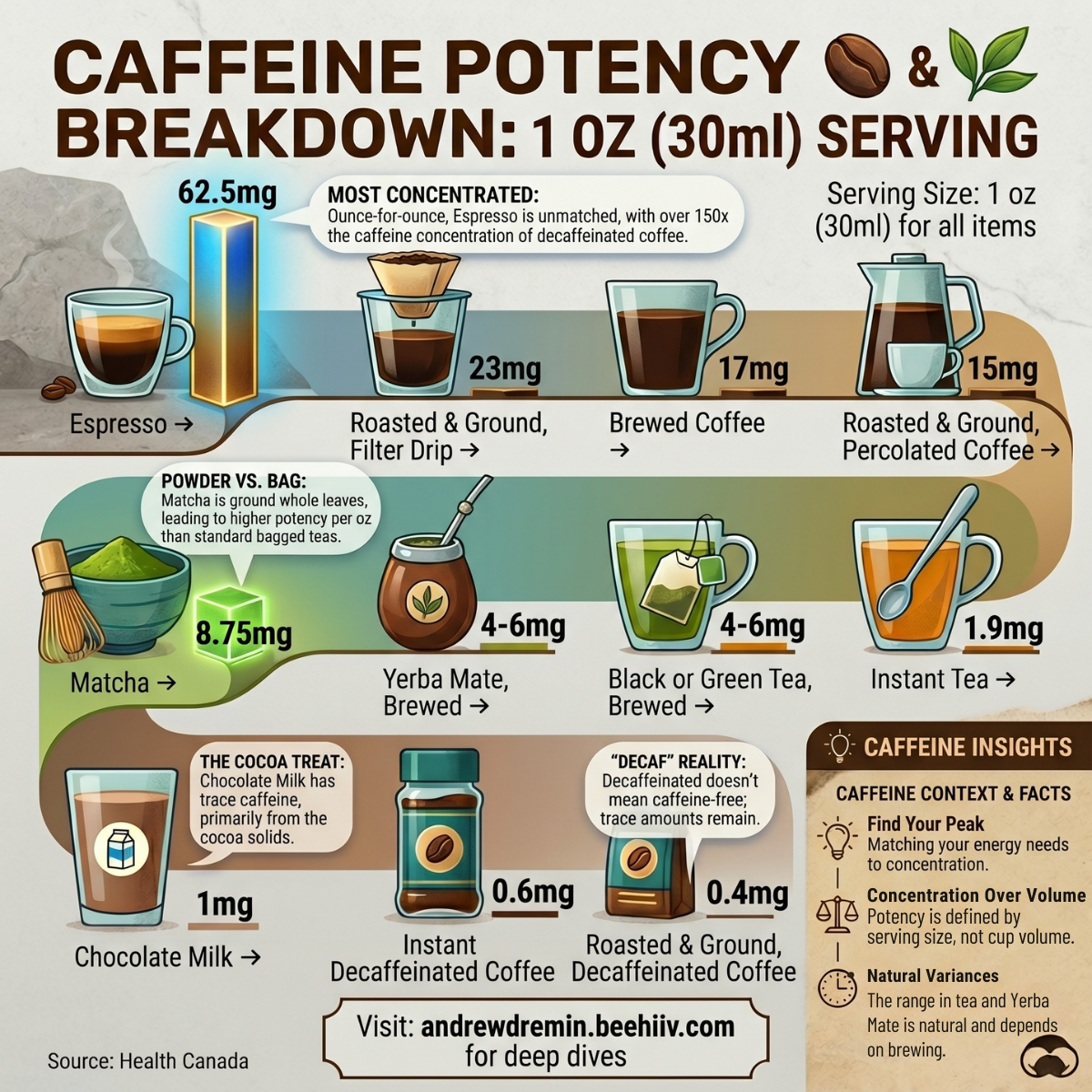

Let’s look at the numbers.

Standard espresso packs 62.5mg of caffeine per single ounce. It is a highly concentrated stimulant. Standard brewed coffee sits at roughly 17mg per ounce.

Now look at a standard canned energy drink. It usually contains around 9.5mg of caffeine per ounce (32mg per 100ml).

Yes. Espresso is over six times more concentrated than the drinks regulators are currently banning.

Yet, global laws heavily target the aluminum cans while leaving the specialty coffee cups completely alone. On paper, it makes no logical sense.

Why does this happen?

I analyze market behavior and regulations daily. Regulators are not just looking at the molecule. They are looking at the consumption mechanics and the physiological delivery system.

Coffee is hot. It is bitter. It requires time. It forces the consumer to sip it slowly. The caffeine enters the system gradually.

Energy drinks are fundamentally different. They are served ice-cold. They are carbonated to speed up absorption. They are loaded with massive amounts of sugar and synthetic flavor masking. A teenager can easily chug a standard 16-ounce (473ml) can in under two minutes. This delivers an immediate spike of 160mg of caffeine, taurine, and a massive insulin shock simultaneously.

That is the real target. It is the speed of consumption, the chemical synergy, and the aggressive marketing appeal to youth.

Take a recent industry example I reviewed. A major European beverage brand was forced to halt a multi-million-euro product rollout. Sudden local compliance updates caught them off guard weeks before launch. They scrambled. They thought the caffeine volume itself was the enemy. They tried tweaking the formula, reducing the milligrams slightly, and relaunching. It failed again.

My professional opinion on this case? The panic was misplaced, and their reaction was tactically wrong. The issue was not just the active ingredient. It was the category classification and the aggressive format they refused to let go of.

The tired consumer standing at the supermarket shelf does not care about regulatory politics. They do not care about the Spanish Health Ministry data or UK parliament debates. They just want a reliable, quick physical boost to finish their factory shift, their delivery route, or their university study session.

But they are reading labels closer than ever before. And parents are actively blocking traditional energy brands from entering the house.

So, what are the conclusions for FMCG and retail leaders?

If you are planning your portfolio for 2026 and beyond, you need a hard pivot.

1. Pivot the format, exploit category exemptions.

Stop launching standard synthetic energy drinks in neon 16-ounce cans. The regulatory net is permanently closing on this format. Instead, allocate R&D budgets to functional ready-to-drink (RTD) coffee and premium steeped teas.

Read the fine print of the new laws. The legislation being drafted right now specifically targets “energy drinks” over a certain threshold (usually 150mg/L). But almost all of them contain explicit legal exemptions for traditional coffee and tea categories. This is your operational loophole.

A functional cold brew or a premium matcha RTD sits comfortably outside the regulatory stigma. Matcha provides roughly 8.75mg of caffeine per ounce. It delivers the precise functional boost the consumer wants, but it is classified differently by the state. You secure the revenue, you eliminate the compliance risk.

2. Shift from “energy” to “focus” and “wellness”.

The word “energy” on a can now attracts immediate regulatory audits. Reposition your products around cognitive focus, hydration, and natural stamina. Sell the outcome, but change the vocabulary. Consumers want endurance, not a synthetic heart-rate spike.

3. Natural ingredients are not a magic legal shield.

I see many brands making this cognitive error. Do not assume that switching from synthetic caffeine to natural guarana extract will save your product from a ban. The laws measure total caffeine volume per liter. If your drink has 160mg of natural caffeine, it will still get banned if it falls under the energy drink legal definition. You absolutely need a clean label for consumer trust, but you also need to exist in a legally safer beverage category. Natural does not mean immune.

4. Review portfolios early and audit your risk exposure.

Do not wait for a local ban to hit your specific operating region. We see the pattern clearly in Spain, Poland, and the UK. It will inevitably spread to other markets. If 70% of your revenue depends on high-caffeine, high-sugar cans marketed to younger demographics, your risk exposure is at a critical level. Start shifting your product mix today. Build a parallel portfolio of functional wellness drinks that can absorb the revenue shock when the energy drink bans hit your country.

5. Rethink retail placement and vending strategies.

With the new regulations, placement is becoming as restricted as the product itself. In several countries, high-caffeine drinks are being pushed out of standard vending machines and banned near schools. If your distribution strategy relies heavily on automated retail or convenience stores near educational hubs, you will lose that shelf space overnight. RTD coffee and functional teas do not face these geographical restrictions. They keep your product at arm’s reach of the consumer.

6. The pricing architecture must evolve.

Energy drinks traditionally rely on high margins driven by cheap synthetic ingredients. RTD coffees and premium teas require real ingredients, which compresses margins. FMCG leaders need to adjust their pricing models now. Consumers are willing to pay a premium for clean, functional beverages that do not carry the junk food stigma. Price your new formats to reflect premium utility, not just cheap volume.

The beverage market is shifting fast. The companies that survive will not fight the regulators. They will simply walk around them by changing the format and the category.

Share your opinion. How do you deal with these rapid regulatory changes in your sector?

Related posts:

The €3.90 Gourmet Threat: How Supermarket Meal Kits are Disrupting Fast Casual Dining

The €3.90 Gourmet Threat: How Supermarket Meal Kits are Disrupting Fast Casual Dining

Inditex Q1 2026 Performance

Inditex Q1 2026 Performance

The Billion-Dollar Illusion: How a Fake Movie Parade Transformed Global Retail and Tourism

The Billion-Dollar Illusion: How a Fake Movie Parade Transformed Global Retail and Tourism

The Small Appetites Economy: How Weight-Loss Drugs Are Rewriting the Rules of Retail

The Small Appetites Economy: How Weight-Loss Drugs Are Rewriting the Rules of Retail

The Supermarket That Wants to Be a Restaurant

The Supermarket That Wants to Be a Restaurant

Lidl is now your phone operator

Lidl is now your phone operator

Leave a Reply