I have spent my career watching the retail wars play out across the globe. Usually, when a company hits a massive milestone, it is all over the news. But on April, 2026, something historic happened in complete silence. The REWE Group officially crossed the €100 billion annual revenue threshold.

For those of us in the industry, this is a “wow” moment. To put it in perspective: REWE is now bigger than the global revenue of Carrefour. While the world focuses on Amazon’s tech or Lidl’s expansion, this German cooperative has built a multi-brand empire across 21 countries without making much noise at all.

How do you build a €100 billion giant that nobody outside Europe has heard of? It comes down to a very specific DNA – a model that chooses local owners over stock market hunters.

Where REWE Stands: The New European Hierarchy

In the past, the “Big Three” of European retail were usually seen as Schwarz Group (Lidl), Aldi, and Carrefour. That has changed. REWE has quietly climbed the ladder and is now firmly in the top tier.

If we look at the latest revenue estimates for the 2024/25 period, the landscape looks very different than it did just a few years ago.

Top European Food Retailers by Revenue (Est. 2024/2025)

| Retail Group | Home Country | Est. Revenue (€bn) | Operating Model |

| Schwarz Group (Lidl/Kaufland) | Germany | €175.0 – €186.0 | Integrated/Private |

| Aldi (Nord & Süd) | Germany | €115.0 – €155.0 (Global) | Integrated/Private |

| REWE Group | Germany | €100.4 | Cooperative |

| Ahold Delhaize | Netherlands | €97.0 – €99.0 | Publicly Traded |

| Carrefour | France | €82.1 – €98.0 | Publicly Traded |

| Edeka | Germany | €75.3 – €82.5 | Cooperative |

| Tesco | UK | €67.0 – €72.7 | Publicly Traded |

Look at those numbers. REWE has moved ahead of Carrefour and is neck-and-neck with global giants like Ahold Delhaize. But unlike Ahold, which gets about 60% of its money from the US, REWE is almost entirely a European story.

The Financial Architecture: Spending Now to Win Later

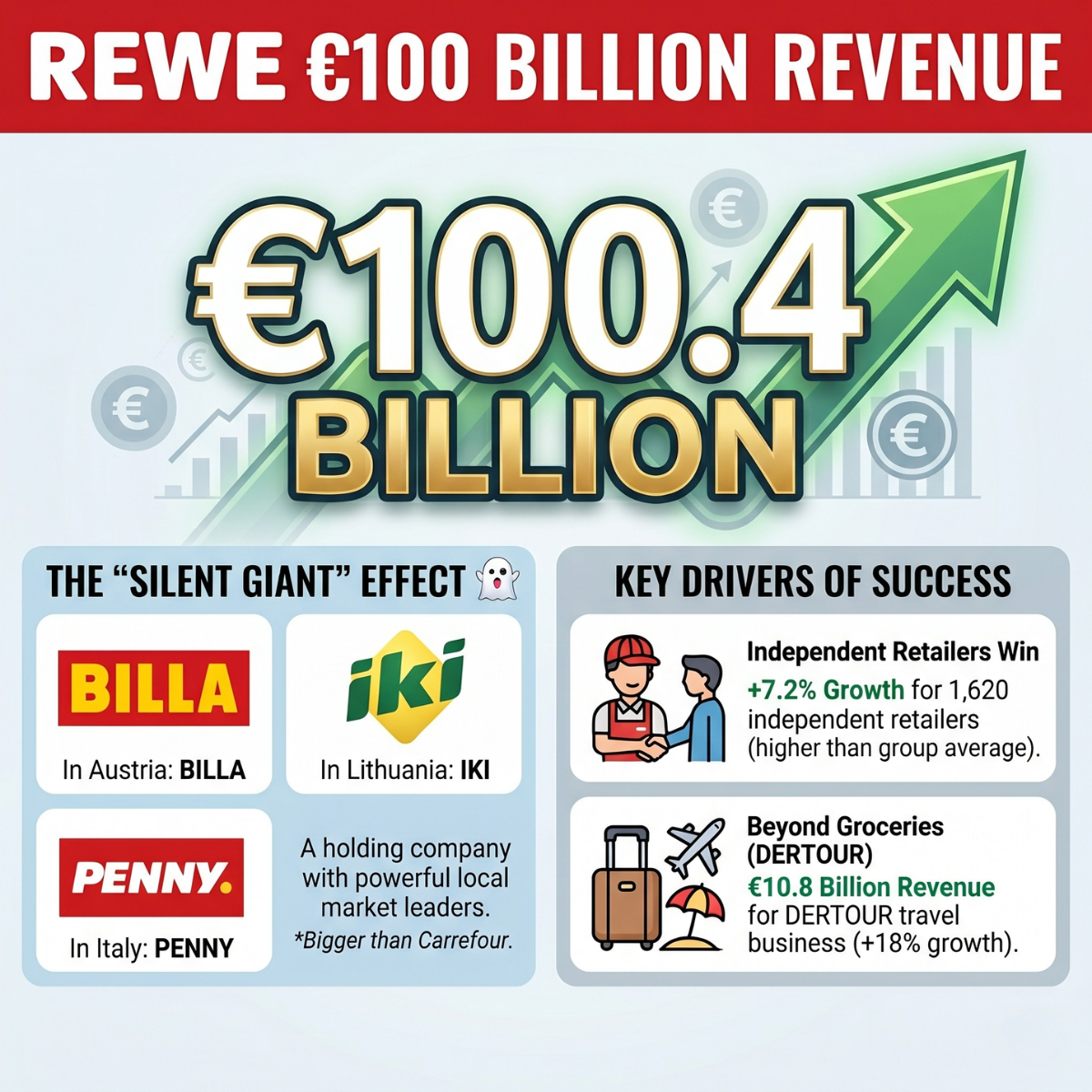

The 2025 financial year was the turning point. It was a tough year for everyone. Food inflation was high, and consumers were very cautious. Yet, REWE increased its total external revenue by 4.0% to hit €100.4 billion.

If you look at the table below, you will see a drop in profit (EBITA). In a public company like Carrefour or Tesco, this would make the stock price tank. But at REWE, this was a deliberate strategic choice. The leadership decided to absorb rising costs and invest billions into the future.

Detailed Financial Performance Indicators 2025

| Metric | 2025 Performance | 2024 Performance | Year-on-Year Change |

| Total External Revenue | €100.4 billion | €96.5 billion | +4.0% |

| Group Revenue (RZF) | €91.1 billion | €87.9 billion | +3.7% |

| EBITA (Operating Profit) | >€1.5 billion | €1.99 billion | -23.3% |

| Net Income | €525 million | €1.01 billion | -48.0% |

| Shareholders’ Equity | €11.6 billion | €11.0 billion | +5.5% |

| Operating Margin (EBITA) | 1.7% | 2.3% | -60 bps |

**Note: 2024 net profit included a significant one-off tax refund effect. *

The group invested €2.5 billion in 2025 into digitalization and logistics. They plan to increase this to €3 billion in 2026. They are betting that being the most advanced retailer is more important than having the highest profit this quarter.

The Cooperative Heart: Why “Local” Always Wins

The reason REWE is so resilient is its structure as a “Genossenschaft” or cooperative. It is not one giant machine; it is a network of approximately 1,620 independent retailers in Germany alone. These people are not just managers; they are entrepreneurs who own their shops.

I once saw a report about a toom Baumarkt (REWE’s DIY arm) retailer named Theodoros Lazaridis. He opened his store near Stuttgart and said the cooperative gives him “security and stability” while letting him lead with his own signature. Another retailer, René Irrgang, who runs two stores in Cologne, uses TikTok and Instagram to be the “favorite neighbor.”

In 2025, these independent REWE retailers outpaced the rest of the group, growing their revenue by 7.2% to €20.4 billion. As a professional, I see this as a lesson: when the person running the store is part of the community, they fight harder. They source from local farmers through the “REWE Local Partnership” and know exactly what their neighbors want. This “personal touch” is their best defense against big discounters like Aldi.

Retail Germany: The Two-Front War

In its home market, REWE has to play two different games. Germany brought in €42.5 billion in retail revenue in 2025.

- The Supermarkets (REWE): These are the flagship stores, numbering about 3,800. They grew 3.0% to €32.4 billion. They focus on “omnichannel” services – connecting physical stores to a strong mobile app and delivery service. Data shows that customers using both physical and online channels increase their revenue contribution by 30% in the long term.

- The Discounters (Penny): This is where the price war is. Penny grew only 0.7% to €9.9 billion in Germany. It is a brutal fight against Aldi and Lidl, but Penny is holding its ground by focusing on fresh food and its digital loyalty app, which now has 7 million users.

They even control their own supply chain with their own bakeries (Glocken Bäckerei) and quality butchers (Wilhelm Brandenburg). This gives them a level of quality control and margin that “middle-man” retailers just don’t have.

International Growth: The Multilocal “Ghost” Strategy

REWE’s international strategy is brilliant because it is humble. They don’t force the “REWE” name on everyone. Instead, they buy or build local favorites.

- Austria: BILLA has been a staple for over 70 years. Along with BIPA (drugstores) and ADEG, the Austrian full-range business made €8.2 billion in 2025.

- Lithuania: IKI is their “innovation playground” where they test high-tech 3D advertising and retail media.

- CEE Momentum: Revenue in Central and Eastern Europe grew by 7.2% to €4.2 billion.

- International Penny: Unlike Germany, PENNY International saw robust 6.3% growth last year, reaching €8.6 billion.

By using local brands, they keep the trust of the shoppers while using the massive “back-office” power of a €100 billion group.

The Secret Weapon: Lekkerland and Convenience

If you want to know how REWE got to €100 billion, you have to look at Lekkerland. Bought in 2020, this wholesale giant is the invisible force behind REWE’s scale.

- The Scale: They supply 62,000 points of sale across Europe—mostly petrol stations and kiosks.

- The Revenue: In 2025, the Convenience segment (led by Lekkerland) brought in €15.3 billion.

- The Tech: Lekkerland is currently rolling out a future-ready Warehouse Management System (WMS) to be finished by 2028. They are automating the “on-the-go” supply chain so they can handle complex, high-frequency deliveries better than anyone else.

- The Synergies: This is why you see “REWE To Go” shops at Aral gas stations. They combine REWE’s fresh food expertise with Lekkerland’s logistics.

Analysts point out that Lekkerland operates on a razor-thin 2% EBITDA margin. This “dilutes” the overall group’s profitability, but REWE is essentially trading profit percentage for massive negotiating power with global suppliers like Mars and Coca-Cola.

DERTOUR Group: Selling Experiences, Not Just Groceries

This is where REWE leaves other grocers behind. They have a massive tourism arm called DERTOUR Group.

While grocery margins are paper-thin, tourism is a growth engine. In 2025, tourism revenue jumped 18.0% to €10.8 billion. REWE CEO Lionel Souque noted that people are spending more on “individual experiences” like tailor-made long-haul trips.

In August 2025, they bought the Swiss Hotelplan Group, making them the leader in the Swiss market. By owning over 2,000 travel agencies and 120 hotels, REWE hedges its bets. If food sales are flat because of a price war, holidays are usually booming.

Tech and AI: Not Just Buzzwords

REWE is ahead of the curve on tech. They are expanding “Pick&Go” stores where you don’t even scan your items. They use computer vision and AI to build a 3D model of the store. You just walk in, take a sandwich, and walk out. There are now seven of these locations in Germany, including a new 650-square-meter site in Hanover.

They are also winning at Retail Media. They have data on 30 million weekly shoppers. By selling ads on their apps and in-store screens through “Retail Media Connect,” they create high-margin revenue. In Austria, BILLA’s screens reach nearly 4.7 million customers per week – about half the population.

The Analyst’s View: Margins, Fines, and Red Flags

But man, look at that 1.7% operating margin. That is a tightrope walk. Analysts at S&P and other firms have raised some yellow flags.

1. The Profitability Gap

REWE’s EBITA margin of 1.7% is lower than Ahold Delhaize or Tesco. Critics argue that REWE is being squeezed by discounters on one side and a resurgent Edeka on the other. S&P has noted that REWE’s cash flow generation lags its peers because its capital spending is so aggressive.

2. Legal Headwinds: The €70 Million Fine

In Austria, the group was just hit with a staggering €70 million fine for “gun-jumping.” They implemented a retail space lease before getting official merger clearance. The Austrian Supreme Court increased the fine 47-fold from the original amount. For a business where net income is only €525 million, a €70 million penalty is a massive hit.

3. The Greenwashing Backlash

REWE recently had to stop advertising its own-brand products as “climate-neutral.” They were using carbon offsetting certificates, which critics called “fake climate protection.” This is a blow to a brand that builds its entire identity on being the “good, local merchant.”

Labor and Reality: Strikes and the Talent War

Like every other retailer in Europe, REWE is fighting a talent war. The CEO has warned of “endless queues” and stores in rural areas closing early because they can’t find staff.

At the same time, they are dealing with labor disputes. The Verdi union has been calling for warning strikes across Germany, demanding higher pay and better rest periods. While REWE tries to automate with Pick&Go to save labor, the reality on the ground is a tense social climate where workers feel the pressure of the cost-of-living crisis.

Why Did the Media Miss the Milestone?

If this was Carrefour hitting €100 billion, it would be a “breaking news” alert. But REWE is a cooperative.

- No Shares: They don’t have a stock price that jumps up and down. No public shares means no headlines for financial reporters.

- Fragmented Branding: Because they are BILLA in one country and IKI in another, the global press doesn’t see one big empire.

- Inward Focus: They are happy staying in Europe. They don’t chase fame in the US or China, so the US media ignores them.

Conclusion: Lessons for the Industry

The rise of this “Silent Giant” gives us three clear takeaways:

- For Retailers: The independent owner model is still the gold standard for growth. Local ownership beats corporate management because owners care about the community.

- For FMCG: You need to be in the Lekkerland ecosystem. With 62,000 locations, it is the most important “on-the-go” network in Europe.

- For SMEs: Scale doesn’t require a global logo. Be useful first, and the revenue will follow.

Leave a Reply