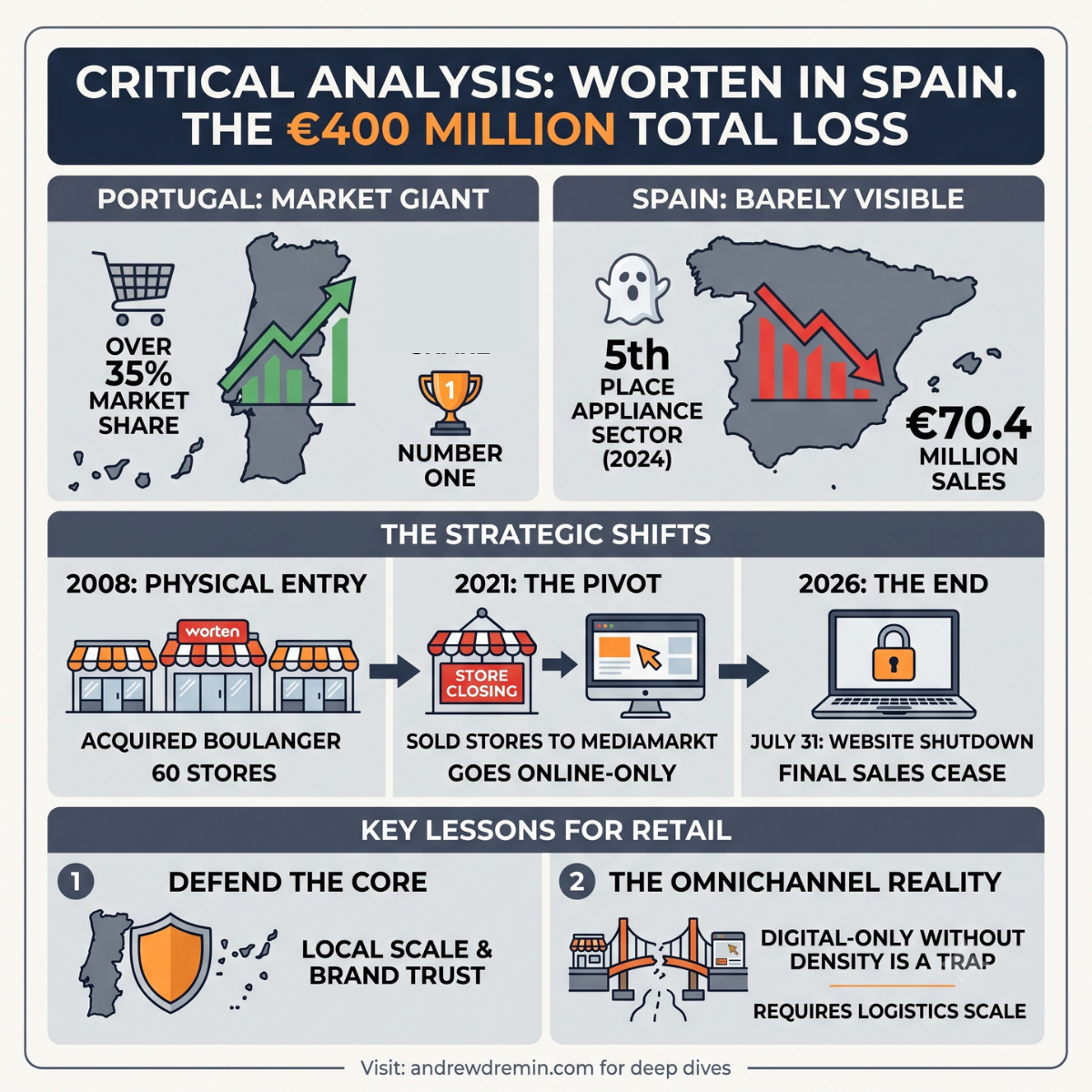

€400 million. That is the estimated total loss Worten España generated in mainland Spain before deciding to pull the plug on its website this coming July 31, 2026.

Blaming Amazon or Temu for killing legacy retail is an easy out. The reality is more clinical: Worten lost an 18-year war of friction against entrenched incumbents and scale asymmetry.

In Portugal, Worten is dominant, holding over 35% of the market. But cross-border retail does not care about domestic success. In Spain, they never achieved critical mass. By 2024, their appliance market share had dwindled to just €70.4 million in sales.

The Financial Bleeding (2008–2020)

Worten entered Spain in 2008 by purchasing the assets of Boulanger. It was an expansion plan built on speed rather than sustainable infrastructure. By looking at their historical financial filings, the structural deficit becomes clear. The brand failed to turn a profit in almost every single year of its Spanish operation.

To understand the size of the failure, look at their historical annual losses:

- 2011: €27 million loss

- 2012: €33 million loss

- 2013: €76 million loss

- 2014: €39 million loss

- 2015: €32 million loss

By 2020, cumulative losses crossed €385 million. The parent group, Sonae, kept injecting capital, hoping that digital changes or local optimization would fix the underlying issue. It did not work.

The Scale Asymmetry

The fundamental problem was structural. In retail, buying power determines your margin. If you buy 10,000 washing machines, you get a much lower price per unit than a competitor buying 500. Worten never matched the procurement scale of Germany’s MediaMarkt.

| Metric (Historical Peak) | Worten España | MediaMarkt España |

| Average Annual Revenue | ~€230 million | ~€1,800 million |

| Store Count | 50–60 stores | 100+ stores |

| Market Position | Low-density challenger | Entrenched market leader |

MediaMarkt locked down the prime, high-traffic retail locations across Spain before Worten could establish a footprint. This created a permanent real estate deficit. Worten was forced into secondary commercial parks with lower foot traffic but high fixed rental costs.

The 2021 Pivot: The Digital Illusion

In 2021, Worten accepted reality. They executed a controlled retreat: they sold 17 of their best physical stores to MediaMarkt, closed another 15, and let go of a large portion of their workforce via an ERE (Employment Regulation File). The remaining operations in mainland Spain went entirely online.

This was not a naive bid to beat Amazon at its own game. It was an operational pivot to salvage brand equity and stop the bleeding of physical overhead.

However, moving entirely online is rarely a cure for a failing brick-and-mortar business. Consumer electronics have thin margins, often between 5% and 10%. When you close your physical stores, you lose your physical touchpoints.

A pure digital model relies on two expensive drivers:

- High Customer Acquisition Costs (CAC): You must pay Google and Meta constantly to drive traffic to your website.

- Heavy Logistics Overhead: Shipping single major appliances – like refrigerators or washing machines – to individual apartments is highly inefficient without a local hub-and-spoke store network.

Without physical stores to support an omnichannel loop – such as click-and-collect or local in-store returns – a standalone regional e-commerce site simply burns cash.

The Marketplace Trap (2024–2026)

To survive online, Worten launched a third-party marketplace. They invited external merchants to sell on their platform, charging them a commission. The catalog grew to over 700,000 products, and by 2024, they brought in €70.4 million in sales.

But a marketplace only works if the platform handles massive traffic. Merchants leave if traffic drops. As Amazon, AliExpress, and local players like PcComponentes squeezed the Spanish digital space, Worten’s traffic acquisition costs became unsustainable.

The end of the experiment was predictable. On June 30, 2026, external marketplace sellers received a brief email. The platform stated it was ceasing all online sales in mainland Spain on July 31, 2026. Sellers were told they can no longer upload products or take new orders after that date.

Currently, the website is running a “Stock Fuera” clearance campaign, offering discounts up to 50% to liquidate remaining inventory. They also announced that the “Worten&go” customer discount program will terminate entirely on July 31. Just like that, a revenue channel vanishes for hundreds of small merchants.

The Strategic Exception: Portugal and the Canaries

Why is Sonae keeping Worten alive in Portugal and the Canary Islands? Because density and structure matter.

In Portugal, Worten is the dominant market leader with massive infrastructure and brand trust. In the Canary Islands, the model is different. Worten operates 24 physical stores there through a joint venture with a powerful local partner, Grupo Número 1. The islands have isolated logistics and different tax structures, protecting them from the immediate friction of mainland e-commerce giants.

If you cannot achieve operational density in a new market, capital is better spent defending your home turf.

The Strategic Takeaways for Retail

- Defend the Core: Do not expand into high-friction regions if your home market requires defensive capital. Sonae learned this after losing €400 million over 18 years.

- The Omnichannel Reality: Moving online to escape brick-and-mortar overhead is not a real pivot. It is usually just a slower way to burn capital. If your digital business lacks a local logistics advantage or proprietary products, you are just an expensive digital storefront.

We need business strategies built on scale and structural defense, not digital illusions.

Moving online to escape brick-and-mortar overhead isn’t a pivot – it’s usually just a slower way to burn capital. If your expansion plan lacks a local density advantage, you are fighting a losing war of friction against entrenched players.

Let’s audit your structural defenses before the market does it for you.

Related posts:

Shrinkflation Communication: Inside Mercadona’s PR Disaster

Shrinkflation Communication: Inside Mercadona’s PR Disaster

Tesco and Football championship

Tesco and Football championship

The Billion-Dollar Illusion: How a Fake Movie Parade Transformed Global Retail and Tourism

The Billion-Dollar Illusion: How a Fake Movie Parade Transformed Global Retail and Tourism

The Big Mistake of Nike

The Big Mistake of Nike

Electronic shelf labels wars

Electronic shelf labels wars

The Small Appetites Economy: How Weight-Loss Drugs Are Rewriting the Rules of Retail

The Small Appetites Economy: How Weight-Loss Drugs Are Rewriting the Rules of Retail

Leave a Reply